5.24.24 Tredas Weekly Recap

Weekly Action:

Corn Jul24 up 12.25 at 465

Beans Jul24 up 22.25 at 1249.5

KC Wheat Jul24 up 64.25 at 725

Hogs Jul24 down 2.80 at 97.325

Fats Jun24 down 3.0 at 183.925

Feeders Aug24 up 8.80 at 260.425

Corn Dec24 up 11.25 at 488.5

Beans Nov24 up 18.0 at 1220.25

KC Wheat Dec24 up 60.0 at 756

Market Recap:

Grains and oilseeds reacted positively to international headlines to start the week and held/added on to those gains into Friday. Thursday and Friday featured low volume trade as markets continue to digest planting progress and sever weather across parts of the corn belt.

CZ24: Since breaking above the 100-day moving average on May 2nd, corn has held a 475-495 range and has struggled to close above the 200 day moving average currently sitting at 493.

SX24: New crop beans are experiencing similar technical support and resistance. There is still a gap in the chart from the first of the year. 1230-1240 levels will be key resistance if we continue rallying into next week.

Updated planting progress report will drop on Monday afternoon.

Snapshot of historical Prevent Plant acres courtesy of Rich Nelson on X:

Another interesting chart from Susan Stroud on X, shows total US area in drought since Jan 2020.

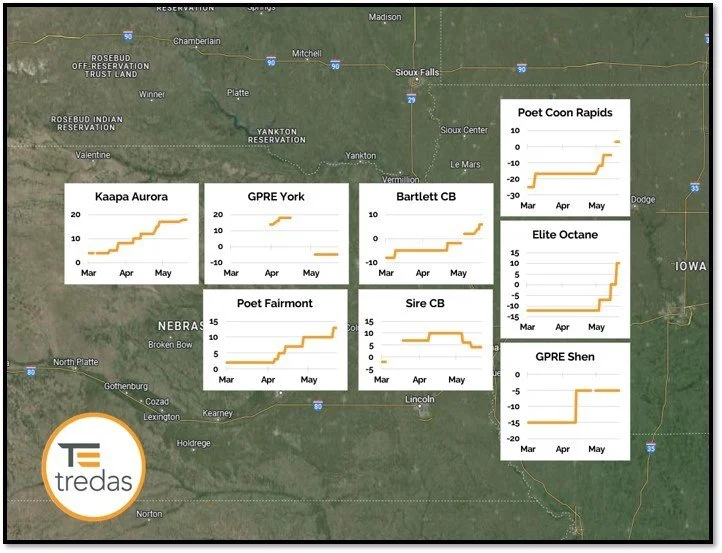

Area Basis:

Here’s a look at June delivery basis values at a handful of destinations in the area. Destinations have generally had to match or improve on May posted values, continuing to show nearby basis premiums compared to the deferred months.

Livestock:

The cattle market extended last week’s rally and surpassed the recent highs from 3 weeks ago. The May Livestock Slaughter report yesterday showed April cattle slaughter was 109% of March and 107% of last year. Fed cattle carcass weights were up 9lbs from March and 22lbs heavier than last year. The Jan – Apr beef production was only slightly below last year on record carcass weights.

Futures prices on Live and Feeders took a pause yesterday and today ahead of this afternoon’s USDA Cattle On Feed report. The average trade guesses for the report were for On Feed as of May 1 to be 99.2% of last year, Placements to be 93.9%, and Marketings in April to be 109.8%. The report showed actual On Feed was 99.1%, Placements were 94.2%, and Marketings were 110.1% .

The cash markets remain strong for live and feeders with retail prices holding firm heading into Memorial Day. Live cattle futures are retesting the highs from Feb/March around $185 and could try to retest the contract highs near $190 in the coming months. Feeder cattle futures need to gain about $10 to retest the Feb/March highs near $270 and are still $20 below the contract highs around $280 so be watching for resistance near those levels moving forward. If we get back near these previous highs this summer we’ll be looking to make hedges, buy puts, and lock in LRP insurance to protect from another correction into fall.

Broader economy:

The stock market hit more highs this week. However, continued strong economic data has reinforced the Fed’s latest stance on interest rates being “higher for longer.”

Something that probably means nothing:

Americans will eat upwards of 800 hot dogs per second on Memorial Day, totaling around 70 million hot dogs consumed.

Quote of the week:

"It is foolish and wrong to mourn the men who died. Rather we should thank God such men lived." –George S. Patton

Thanks and have a great weekend!