Tredas Recap 7.26.24

Weekly Action:

KC Wheat Sep24 down 27 at $5.46

Corn Sep24 up 3 at $3.95

Beans Sep24 up 4 at $10.40

Hogs Oct24 up 3.65 at $78.15

Fats Oct24 up 5.225 at $188.50

Feeders Sep24 up 3.675 at $259.20

Corn Dec24 up 4 at $4.10

Beans Nov24 up 11 at $10.47

Market Recap:

Very little new information hit the marketplace this week. We are in the dog days of summer and some areas of the country have tremendous potential and some areas are ready for next year.

With that being said, last weekend, several Tredas brokers had the opportunity to attend the RJO Introducing Brokers Conference where we discussed several different commodities and opinions on future price action. No one knows the future, but the following should be interesting slides/data points/perspectives for you to ponder over the weekend.

It seems a common grumbling point among farmers is row crop prices aren’t keeping up with inflation. We are not in a position to answer that, but someone at the conference presented the information below. It shows the national cash index vs average production cost in the United States. A 1.00 rating would be cash corn equaling the cost of production that year.

According to him, the national average cost to grow corn this year is $906/acre. From 2016-2020 the average cost was $707/acre. This is a 28% increase (inflation). His philosophy was if you took around a $4.20 December 2024 board price and deducted inflation you would be very close to $3.00 December 2016-2020 equivalent board price, which was about where the sustained lows were during this time. With the same math you would be around a $8.00 November 2016-2020 equivalent board price. So, in his eyes, row crops have kept up with inflation when factoring in a large crop on the way and projected stocks/use similar to the 2016-2020 period. Corn stocks/use during that period ranged between 13.7-15.7%. USDA is currently projecting corn stocks/use to be 14.1% this year.

***This does not mean we cannot go lower before harvest.

Below is both ending stocks and stocks/use for corn in America. The projection for this year is around a 2.1-billion-bushel carryout and 14.1% stocks/use. So far this year, we are comfortably within the range of both carryout and stocks/use as the 2016-2020 period.

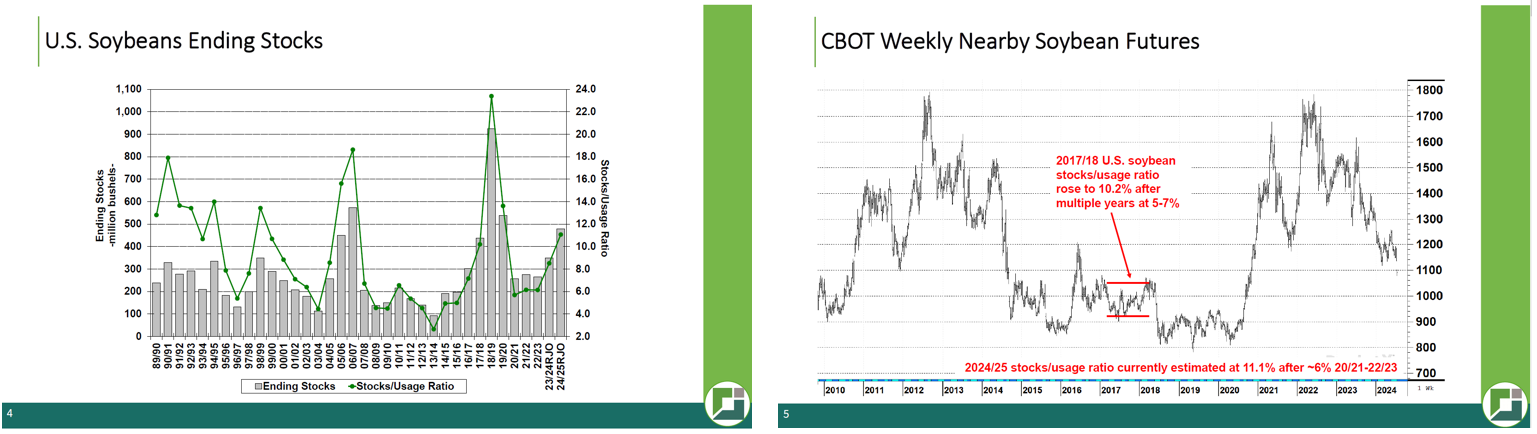

Current USDA projections have this year’s U.S. soybean carryout at nearly 500 million bushels and a 11.1% stocks/use. The good news: this isn’t even close to the China tariff days when ending stocks were record high above 900 million bushels and stocks/use a wild 23%. Back to the inflation math, the current November soybean board is “basically” at the 2019/2020 lows.

Wheat ending stocks and stocks/use are still well below the 2016-2020 level, as is price. For those of you who had to deal with $4.00 futures and negative basis during that time frame, you know as a wheat farmer “it could always be worse”. The RJO commercial presenter believes the USDA may raise Kansas HRW from 43 to 50 by the time they are done with this crop. We will see how it ends up. The Spring Wheat crop tour is projecting large yields also.

When discussing cattle, a common topic has been the size of the cow herd and calf population. This is being seen in June 1st COF as we are about 1 million head on feed fewer than just a couple years ago. One thing to keep in mind, though, is carcass sizes are well above the 5-year average as cheap inputs and high live prices are incentivizing longer time on feed. With that in mind, beef production for the month of June was 2.14 billion pounds, which is down 9% from a year ago. Beef 90% trimmings have been on a tear but notice the value difference between domestic trimmings and imports. Look for a continued rise in beef imports.

Weather:

Weather models through next Friday has some indications of better chances of rain through most of Iowa and Illinois and parts of eastern Missouri. (Bottom left) Overall, though, we will be above normal temps in much of the US through the first week of August. (Top Left) New weather models this morning, especially from the European models, suggest if we have tropical weather developing starting around Aug 9 the Eastern Corn belt could see a slightly cooler and wetter pattern. The much above normal temps will also be concentrated over the Rockies and far western plains. This is a slightly more friendly forecast than previously thought earlier in the week. Confidence in the models are not high; mainly depending on an active LH Aug tropical pattern developing. More consistent forecasts will likely come out first of the week. Info courtesy of BAMWX.COM

Economy:

During a Congressional Hearing this week, the CVS Caremark CEO acknowledged the pharmacy charges $6,229 for a drug to treat Multiple Sclerosis. Their cost: $16, which is a 38,000% markup.

This week, Ford Motor reported earnings fell 35% in Q2, which is obviously not good. The kicker: the company actually increased revenue but is starting to realize losses in their electric vehicle business. The company is predicting up to a $5 billion loss from the EV division just in 2024. The stock plunged more than 18% in one day. Tesla also reported a 40% decrease in earnings per share in Q2.

So far, around 35% of the the S&P 500 has reported earnings. Operating earnings are up 4% over the past year, which marks the 6th consecutive quarter with positive YoY growth.

There are nearly 300,000 homes for sale in the Southern Region of the U.S, which is an all-time high. Insurance rates are reportedly the main driver of this as people can no longer afford a vacation home/condo or AirBnb. Other areas of the country are less affected as the U.S. home sale price surged to $397,954, which is a 5% increase since last June.

U.S. GDP last quarter was reported at 2.8% vs the 2.0% estimate and 1.4% last year. The U.S. economy has now been in an expansion for 51 consecutive months with annualized real GDP growth of 4.5% over that time. The U.S. Money Supply also grew 1% over the past year, which is the biggest YoY increase since October 2022. This is not friendly to those wanting rate cuts.

Something That Probably Means Nothing:

It was reported there were just 11.1 births per 1,000 people according to the CDC. That is a 53% reduction from 1960 when there were 23.7 births per 1,000 people.

If you live in a 1,000-person town, this is a decrease of 126 school kids from 60 years ago, or about 10 kids per grade.

Quote of the Week:

“A lifetime of training for just ten seconds.” – Jesse Owens (USA Track & Field, 4-time Olympic gold medalist)

Enjoy your weekend!