12.6.24 Tredas Recap

Weekly Action:

March25 Corn up 7 at $4.40

Jan25 Beans up 5 at $9.95

March25 KC Wheat up 10 at 5.52

Feb25 Hogs up 1.15 at $87.475

Feb25 Fats down 2.60 at $186.025

Jan25 Feeders down 3.325 at $256.15

Dec25 Corn up 5 at $4.36

Nov25 Beans down 6 at $10.06

July25 KC Wheat up 10 at $5.67

Grains:

The December WASDE is next Tuesday. Historically, this report does not include any spicy news. US crop production will not be changed and will be addressed in the in the January 10 Annual Crop Production report. Demand may be revised as well as global crop estimates, if needed.

Below are notes from RJO’s Randy Middlestat:

Corn:

With the pace of U.S. corn export sales and corn for ethanol usage running impressively strong over the last couple months, prospects USDA will raise 2024/25 demand estimates, therefore lowering ending stocks ideas, in this month’s WASDE report certainly are elevated. That said, it is still early in the marketing year and with the favorable early South American growing conditions and the increasing uncertainty over U.S. biofuels policy under the incoming Trump administration, USDA may be more conservative on revisions at this time than a straight-forward look at the data may imply.

Since the start of the 2024/25 U.S. corn marketing year, the pace of export sales has been near record strong, with total combined sales over the first 13 weeks of the year of 846 million bushels being the 2nd highest for the period in available data going back 40 years. Additionally, total export commitments of 1.346 billion bushels already reflect 58% of the USDA’s current 2.325 billion bushel export projection, well above the last two years’ late November sales representing 44% and 45% of eventual annual exports and the average of 46% over the last 10 years. In this context, an increase in the USDA’s export projection certainly is warranted and one we feel they will make this month but could be a bit on the conservative side with the considerable unknowns of export prospects as the marketing year progresses given the favorable South American weather so far supporting prospects for a notable rebound in Argentine production with planting well advanced, as well as being initially favorable for Brazilian safrinha production prospects, as well. Additionally, there is obviously considerable trade uncertainty with President-elect Trump’s threats of the return of notable import tariffs and the potential retaliatory impact that may have on U.S. exports, as well as China’s continued shunning of U.S. corn as they have bought virtually none so far this year vs purchases a year ago of 1.4 MMT by late November and eventual marketing year total exports to China of 3.0 MMT in 2023/24. Given the pace of sales so far, with the increased sales programs to Mexico and the EU vs last year, we are estimating 2024/25 U.S. corn exports at 2.400 billion bushels for now, 75 million above the USDA’s 2.325 billion bushel estimate but would not be surprised if USDA only modestly raises their projection this month by 25-50 million bushels.

Soybeans:

Similar to corn, the pace of U.S. soybean export sales since the actual start of the 2024/25 marketing year September 1 has been near record strong, potentially in reaction to tariff concerns under the new Trump administration as global buyers purchase and ship ahead the January 20 inauguration. While total export commitments are modestly above year ago levels, given the trade policy uncertainty and increasing likelihood Brazil will see a record crop this year and total South American production could increase 20+ MMT from last year, the USDA’s willingness to raise their export projection at this time certainly is debatable.

Since the start of the 2024/25 marketing year September 1, total combined soybean export sales over the first 13 weeks of the year of 860 million bushels are the 2nd largest on record, clearly indicating USDA could feel the need to raise their export projection given the very impressive sales pace so far. However, the fact remains that despite the very strong sales of late, total commitments of 1.330 billion bushels still represent 73% of the USDA’s 1.825 billion bushel export projection, comparable to the late November/annual exports relationship the last two years of 70% and 72% and generally in line with the most-recent 5-year average of 70.1%. Moreover, while total commitments are currently 12% above year ago levels, the USDA’s 1.825 billion bushel export projection reflects an expected 8% increase from last year already so total sales so far are not much out of line with the USDA’s estimate. Despite the very strong sales of late, we do see the window of opportunity for U.S. soybean sales closing given the continued favorable South American weather situation and, particularly, in light of the recent notable weakness in Brazilian export premiums for Feb-forward shipment. In addition, obviously the risk of tariffs and Chinese trade tensions could/should limit sales to China relative to recent-year levels, as well. We feel the longer-term concerns must be kept in mind for now, while the level of sales on the books does not require an upward revision in annual export projections yet. In fact, we are maintaining our ideas 2024/25 U.S. soybean exports could ultimately fall a bit short of the USDA’s 1.825 billion bushel projection as we’re using 1.800 billion bushels in our balance sheet for now.

Wheat:

It could be another rather quiet WASDE report for the U.S. wheat balance sheet as the pace of export sales through the first half of the 2024/25 marketing year has largely tracked with the USDA’s annual export projection while USDA is unlikely to make any material domestic demand-related revisions this month with the next quarterly Grain Stocks report due out in January.

Having reached the halfway point of the 2024/25 U.S. wheat marketing year, total export commitments of 571 million bushels are up a solid 19% from last year’s 479 million, while sales over the last seven weeks have averaged 15.7 million bushels/week vs 12.2 million/week during the same period last year. There may be a bit of protectionist buying going on for U.S. wheat of late as we see potentially/likely being the case for corn and soybeans, as well, ahead of the new Trump administration taking office next month. Prior to the respectable pace of sales over the last seven weeks, total commitments were up 17% vs last year, exactly in line with the USDA’s projected increase in annual exports but has risen slightly to +19% vs last year currently. Additionally, we estimate wheat sales would need to average roughly 8.8 million bushels/week during Dec-May to reach the USDA’s 825 million bushel export projection, modestly higher than last year’s 7.9 million/week average, mostly comparable to the sales gains seen so far. Moreover, current sales on the books represent 69% of the USDA’s annual export projection, slightly above, but not materially so, from the 67% average late November commitments/annual exports relationship of the previous four years. While a notable reduction in Black Sea region (Russia/Ukraine) wheat exports vs last year is going to be seen during Feb-June as a result of the reduced export quotas put in place following this year’s relatively poor crops, harvesting of the Australian and Argentine crops are well underway with solid increases vs last year expected for both, providing at least a partial offset to reduced Black Sea exports. All these factors leave us expecting USDA to hold the line on their 825 million bushel export projection this month. That said, we’re maintaining our 2024/25 U.S. wheat export projection slightly above USDA at 850 million bushels.

Cattle:

The US cattle herd is the smallest its been since 1951, beef production is increasing?

The United States is the world’s largest producer and consumer of beef. The US is also the second largest importer and fourth largest exporter of beef.

Heifer slaughter has remained constant at 8.3 million head/year, while cow slaughter has decreased 15% to only 4.7 million head/year. The reduction in cow slaughter has reduced the intensity of the US destock but has not stopped it entirely. Year-to-October the female slaughter rate (FSR) ran at 49.7%. While this is below the 51.4% during the first 10 months of 2023, it is above the 47% “tipping point”. We have been above this mark since mid-2021.

Despite lower slaughter numbers, overall beef production in the US has increased for the year-to-October by about 0.3% as increases in carcass weights replace lower numbers. Beef production from steers is up 9%. During October, US steer carcass weights averaged around 950 pounds, which is a record. This is about a 30-pound increase from October 2023.

Weather:

South America continues to experience near ideal weather to grow a big soybean crop. Normal rainfall is forecast for Norther Brazil and most of Southern Argentina. Above normal rainfall is expected in Southern Brazil and Northern Argentina. Mostly moderate temperatures are also expected. Soybeans in Northern Brazil are entering pod-filling stage.

The Central Plains are expected to be dry next week. The Southeast may have scattered showers.

Economy:

This week, OPEC+ agreed to extend its 2.2 million barrels/day decline by three additional months. Several members of the alliance are volunteering an additional production cut. Saudi’s energy minister said OPEC+ had to face a “reality check” and wrestle with the supply-demand signals. He said, “There are so many other things, you know, growth in China, what is happening in Europe, growth in Europe … what is happening in the U.S. economy, such as interest rate, inflation,” the Saudi energy minister said Friday. But honestly, the primary cause for moving, or shifting, the bringing of these ballots is [supply-demand] fundamentals. It’s not a good idea to bring volumes in the first quarter.”

US shale oil production crossed 1 million barrels/day in 2011. Since then, Saudi’s market share has been declining. Saudi Arabia will soon have a choice: maintain $60+ price and see market share erode, or increase production to the point it forces others out of the market.

November payroll data was released today. Nonfarm payrolls increased 227,000, but the unemployment rate rose to 4.2%, which was expected. The jobless figure rose as the labor force participation rate decreased and the labor force itself declined. A broader measure that includes discouraged workers and those holding part-time jobs for economic reasons moved slightly higher to 7.8%. Traders speculative this gives the FED a green light to lower rates later this month.

Online sports gambling has become more and more popular, but who is this good for?

SMU studied more than 700,000 accounts and found fewer than 5% withdrew more money than they deposited. These few players collectively won more than $100 million. The next 80% of bettors made up for those operators’ losses. Just 3% of bettors who lost the most represented almost half net revenue. A spokesman for Gamblers Anonymous stated before 2020, a person in their 40s would likely be the youngest person attending a meeting. Today, it is the most common age range.

Something that probably means nothing:

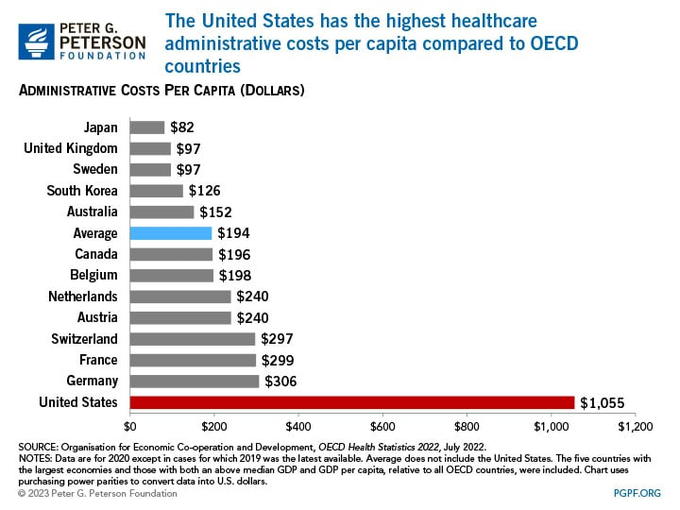

41% of US adults have some form of medical or dental debt from either their personal needs or from a family member.

Healthcare expenditures in the US is $12,500/person, which is about $4,000 more than any other high-income nation.

The leading cause of bankruptcy in the US is from medical debt.

Quote of the Week:

“To appreciate the beauty of a snowflake it is necessary to stand out in the cold.” – Aristotle

Enjoy your weekend!